Automobile Affordability Calculator What Can You Afford?

Recent Auto Loan Rates

We publish an auto lender review guide to help buyers see current rates from top nationwide lenders.

For your convenience, here is data on what rates looked like across Q1 of 2023 after the Federal Reserve likely completed most of the current hiking cycle.

| Borrower | Credit Score | New | Used |

|---|---|---|---|

| Super Prime | 781 - 850 | 5.18% | 6.79% |

| Prime | 661 - 780 | 6.40% | 8.75% |

| Nonprime | 601 - 660 | 8.86% | 13.28% |

| Subprime | 501 - 600 | 11.53% | 18.55% |

| Deep Subprime | 300 - 500 | 14.08% | 21.32% |

Source: Experian 2023 Q1 data

Here were what rates looked like in Q2 of 2022.

| Borrower | Credit Score | New | Used |

|---|---|---|---|

| Super Prime | 781 - 850 | 2.96% | 3.68% |

| Prime | 661 - 780 | 4.03% | 5.53% |

| Nonprime | 601 - 660 | 6.57% | 10.33% |

| Subprime | 501 - 600 | 9.75% | 16.85% |

| Deep Subprime | 300 - 500 | 12.84% | 20.43% |

Source: Experian 2022 Q2 data, published in August of 2022

For historical comparison, here is what the data looked like in Q1 of 2020 as the COVID-19 crisis spread across the United States.

| Borrower | Credit Score | New | Used |

|---|---|---|---|

| Super Prime | 720 or higher | 3.65% | 4.29% |

| Prime | 660 - 719 | 4.68% | 6.04% |

| Nonprime | 620 - 659 | 7.65% | 11.26% |

| Subprime | 580 - 619 | 11.92% | 17.74% |

| Deep Subprime | 579 or lower | 14.39% | 20.45% |

Source: Experian 2020 Q1 data, published on August 16, 2020

Across the industry, on average automotive dealers make more money selling loans at inflated rates than they make from selling cars. Before you sign a loan agreement with a dealership you should contact a community credit union or bank and see how they compare. You can often save thousands of dollars by getting a quote from a trusted financial institution instead of going with the hard sell financing you will get at an auto dealership.

If our site helped you save time or money, please get your accessories like cell phone chargers, mounts, radar detectors and other such goodies from Amazon.com through our affiliate link to help support our site. Thank you!

Look at the Full Cost of Ownership

Purchasing a vehicle is an important event in a person's life. Cars are often the most or second-most expensive thing a person owns depending on whether they own a home or not. However, some people neglect to realize than the sticker price of a vehicle is not the whole cost. There are several different hidden costs involved in owning a car that are not optional and can add up to a significant amount of money.

Beyond the Sticker Price

The sticker price of a vehicle is not anywhere near the total cost of ownership (TCO) or what it actually costs to own a given car. More importantly, it does not always correlate well with the TCO. Some cars can have a cheaper sticker price and still be more expensive to own over a five-year period than a car with a higher sticker price. These are some important hidden costs to consider when buying a car:

- Taxes and Licensing

- Loan Interest

- Depreciation

- Maintenance

- Insurance

- Fuel

Taxes and Licensing

The very first things that most people will pay for beyond the sticker price of their vehicle are taxes and licensing. These costs vary from state to state but will add a national average of 5 percent in sales tax and additional licensing and registration fees. Taxes are a one-time cost but vehicles have to be re-registered every year in most states.

Loan Interest

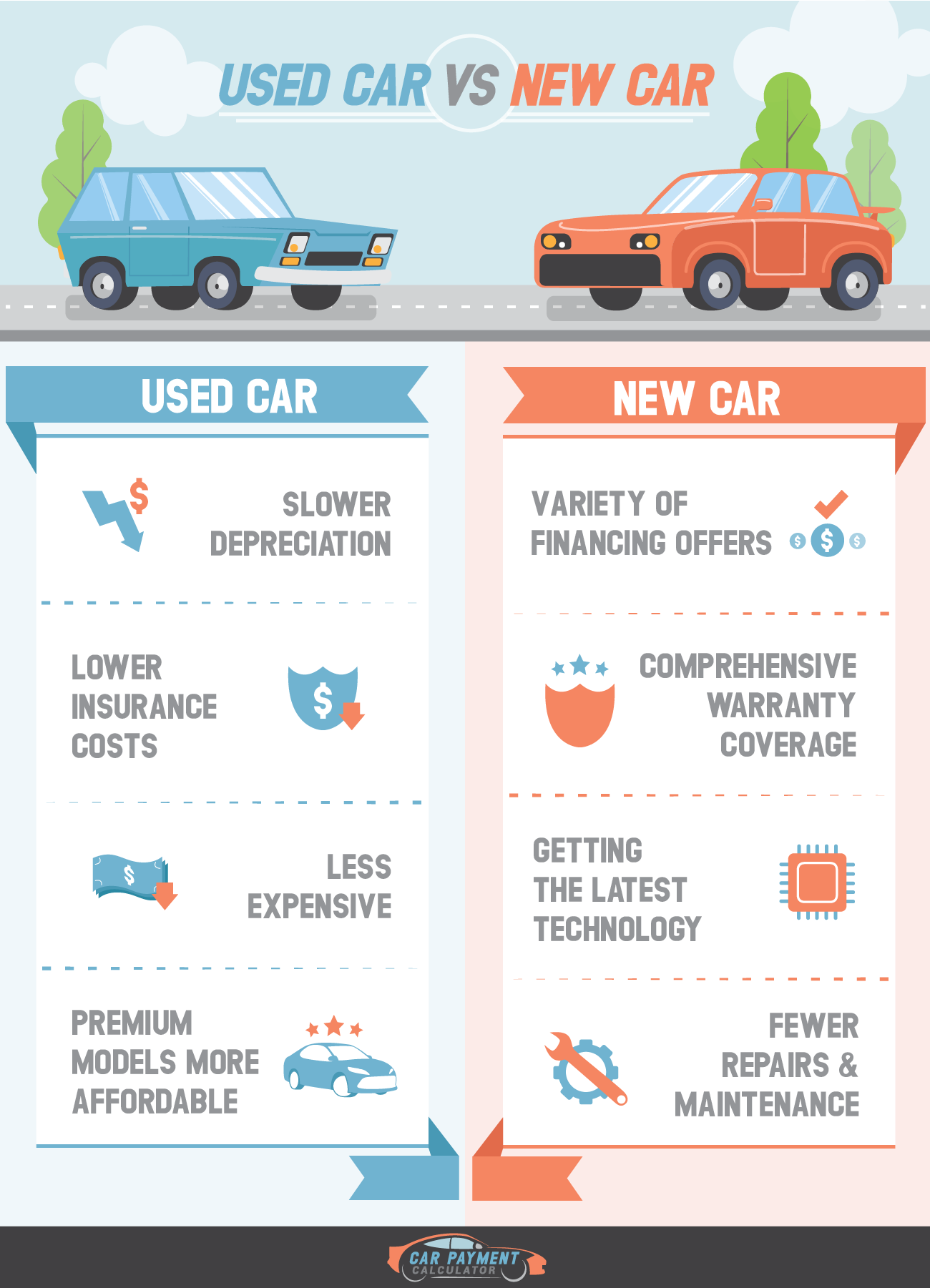

Most people take out a loan to purchase a new car. A smaller but still significant portion of people take out a loan to purchase a used vehicle. The interest rate on loans varies depending on a person's credit history and other factors but it always represents an additional cost that must be figured in to the car's true cost of ownership.

Using the national average interest rate of 6 percent and a down payment of 15 percent, the five-year cost of loan interest makes up 11 percent of the car's true cost to own. The actual cost involved depends on the value of the car purchased since loan interest is calculated as a percentage. It is important to note that the 11 percent is based on total ownership costs during the first five years, not the car's sticker price.

Depreciation

All vehicles depreciate, or lose value, as they age. There are two major types of depreciation that affect the value of cars. One occurs as soon as a vehicle is purchased and the other occurs more gradually over time. A good rule of thumb is that a used vehicle is worth 80 percent of what it was worth one year previously. However, in most cases new cars depreciate much more quickly during their first year than at any other point.

Depreciation After Sale

As soon as a new car is driven off the lot it is no longer worth as much as it was. This is because buying a car from a dealer involves paying the retail price and as soon as the vehicle has changed hands it is only worth the wholesale price. While the vehicle itself is no different than it was on the lot it is only worth what someone is willing to pay for it, which has gone down considerably. Estimates for this loss of value are as high as 20 percent.

Gradual Depreciation Over Time

Cars lose value over time for many reasons. These are some of the most common reasons that older cars are worth less than newer ones:

- Increased maintenance costs

- Reduced reliability

- Increased frequency of repairs

- More expensive repairs

- Shorter useful life

- Lower resale value

Older cars are more likely to need repairs and these repairs are more likely to be expensive. They have fewer years of working life ahead of them than they did when they were newer as well. Mileage has a significant effect on the depreciation of newer cars because most parts wear out based on a combination of age and wear. Older cars which are likely to have parts failing because of age are less affected by depreciation due to mileage but it does still matter.

Depreciation rates vary based on the vehicle type as well. Certain brands have reputations for making long-lasting vehicles and this means that they depreciate less rapidly. Vehicles that have spotty reputations for reliability or other problems associated with them will tend to depreciate more rapidly.

Cars lose significant value through depreciation. A good value for a car is one that depreciates only 40 percent in five years. Depreciation makes up almost half of the total cost of ownership for buyers of new cars over the first five year period and a significant portion of the total cost of ownership for buyers of used cars.

How Depreciation Affects Buyers

Car owners are affected by depreciation in different ways based on how they use their vehicles. Depreciation is of least importance to people who purchase their cars new and drive them for more than five years or purchase them used. It is most important to people who purchase new cars and resell them within five years.

Vehicles depreciate the most during the first year so the loss a person takes on selling a one-year old car is more than the loss a person takes on selling a five -year-old car. All vehicles depreciate but this is only important for people who intend to sell them. Depreciation is of little importance to the driver who purchases new cars only after having driven his or her old one into the ground.

Maintenance

All cars require maintenance in order to remain functional. However, the cost of maintenance differ based on the age and type of car. More expensive cars tend to have more expensive maintenance costs but this is not always the case.

Factors that can increase the cost of maintenance include:

- Rare or hard to find parts

- The use of specialized materials

- The use of premium engine fluids

- A need for high-end tires

- Obtaining service in an area with a high cost-of-living

Cost of Parts

Almost every car will need to have minor parts replaced at some point. If these parts are mass-produced and readily available they will be significantly cheaper than if they are made to order and difficult to find. More expensive cars tend to have more expensive parts but rarer vehicles can also cost more to repair than a more popular vehicle of the same price. Parts for vehicles that are not as popular are harder to find and cost correspondingly more.

Tires are not usually considered part of the cost of maintenance but they do need to be replaced regularly in order for a vehicle to be safe to drive. The cost of tires can vary depending on what kind of vehicle a person drives and what their driving habits are like. Tire prices also fluctuate based on the cost of natural rubber.

Cost of Service

The national average cost of vehicle maintenance in the U.S. is $84 per hour. However, location has an important effect on the fees of service shops and mechanics. Areas with higher costs of living force mechanics to charge more in order to pay their own bills while areas with lower costs of living forces mechanics to keep prices down in order to be competitive.

Why Maintenance Should Not Be Skipped

Overall, maintenance makes up a relatively small part of a vehicle's cost of ownership and there are good reasons not to skip a service. It is important for owners to maintain their vehicles or they could risk voiding their warranty. Cars that were not properly maintained are almost certainly worth less when it comes time to resell as well.

Insurance

In almost all U.S. states there is a minimum amount of liability insurance required in order to drive on public roads. States that do not require insurance require proof of financial responsibility in some other form such as a bond. Insurance can be a major expense for car owners and how much it costs varies based on several factors. Some of the major ones are:

- Age

- Gender

- Marital status

- Driving history

- Type of vehicle

- Number of miles driven per year

- Location

- Multiple-car or multiple policy discounts

Owner Profile

Liability insurance costs are based on the owner profile. This includes age, gender and driving experience. People who can expect to pay more for insurance usually:

- Are younger than 25 or older than 70

- Are male

- Are single

- Put a lot of miles on their cars

- Live or drive in an insurance-industry risk-zone

- Have a history of accidents or tickets

- Drive luxury or expensive vehicles

- Have a poor credit history/score

People who can expect to pay less for insurance usually:

- Are between 25 and 70 years old

- Are female

- Are married

- Drive fewer miles

- Live in an insurance-industry safe-zone

- Have a clean driving record

- Drive less expensive vehicles

- Have a good credit rating and score

These are generalizations and many single men pay less for car insurance than married women. However, most young drivers pay more because they do not have an established driving history as well as being statistically more likely to get into an accident. Tickets and accidents can increase insurance costs considerably for a period of time after they occur but most are eventually considered irrelevant.

Young men, especially young single men, tend to get into more accidents than young women and this is reflected in higher insurance rates. Personal driving experience and a person's driving record also affect the cost of insurance. New drivers are more likely to get into an accident than more experienced ones. People with accidents or tickets on their driving records are more likely to be ticketed again or get into another accident.

People living and driving in certain areas may be at a statistically higher risk of getting into an accident which can affect insurance rates. Insurance rates for a person with the same statistics can vary by more than 500 percent between areas of the country. Although it may not seem relevant, most insurance agencies also consider a driver's credit score. It has been shown to be a solid predictor of future insurance claims.

Insurance costs are based on statistics that certainly do not fit everyone. Unfortunately, insurance companies do not assess people individually when determining coverage charges. There are opportunities for responsible individuals to lower their insurance costs by completing safety courses or maintaining a high GPA at some insurance agencies, however.

Vehicle Profile

The vehicle a person drives helps to determine their cost of insurance in several ways. These include:

- Rate and type of injuries sustained in an average accident

- Typical damage sustained in a crash

- Cost to repair

- Likelihood of being stolen

- etc

Features like how safe a vehicle is can affect liability insurance rates as well as comprehensive and collision coverage. Comprehensive and collision coverage pay the vehicle owner in the event that their car is damaged. These are optional types of coverage but may be required for people who take out loans in order to purchase their vehicles.

Comprehensive and collision coverage costs are based on the value of the vehicle. The age and type of the vehicle has a significant effect here as most people can imagine. Pricier and newer cars are more expensive to insure than older or less expensive vehicles.

Fuel Efficiency

One of the major ongoing expenses involved with owning a car is the fuel. Fuel efficiency is commonly talked about in regards to environmental effects but it also has a significant effect on your wallet. Vehicles vary widely in terms of fuel efficiency and what would be enough gasoline to go a hundred miles in one car might only be enough for twenty-five miles in some trucks or SUVs.

Type of Fuel

Certain vehicles require midgrade or higher fuel. This can add significant costs over a five year period of purchasing gasoline that is ten to twenty cents more per gallon than the basic option. Not purchasing the proper gasoline can cause even pricier problems though, such as soot buildup on turbochargers in vehicles that are equipped with them.

Assessing Hidden Costs

Figuring out whether a certain car is affordable involves a lot more than looking at the sticker price. Factors such as depreciation, fuel costs, insurance rates and maintenance costs must be considered when comparing options. Assessing a vehicle's true cost of ownership allows potential buyers to make a realistic decision about whether they can afford to purchase the car or not.